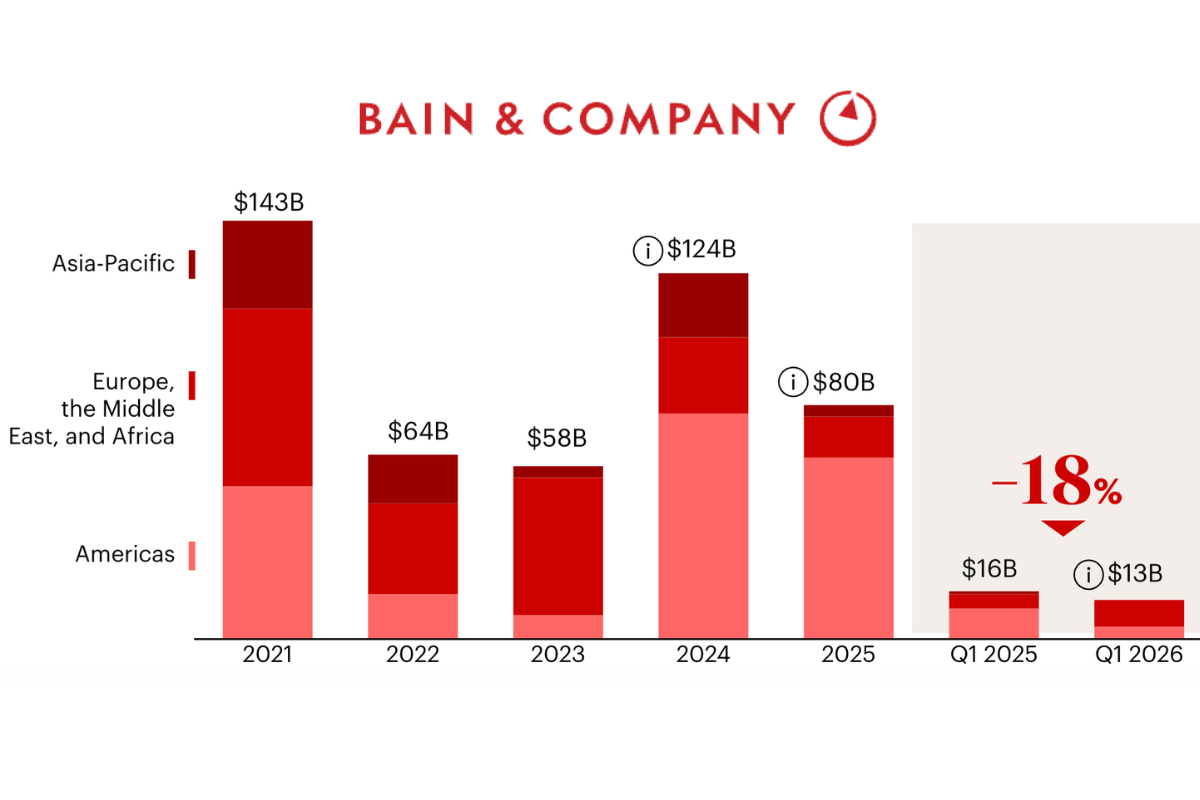

Global telecom merger and acquisition (M&A) activity remained under pressure in the first quarter of 2026, with deal value declining 18% year-on-year as operators continued to prioritize asset sales, portfolio optimization, and infrastructure-focused investments over large-scale acquisitions.

The report suggests that telecom operators across the world are becoming increasingly cautious when it comes to pursuing large acquisitions instead, many companies are focusing on improving balance sheets, simplifying operations, and unlocking value from existing assets.

The telecom sector is facing several external pressures that are making major transactions harder to justify high interest rates remain one of the biggest hurdles with borrowing costs staying elevated in many markets, financing large acquisitions has become more expensive at the same time, uncertainty surrounding global trade policies, tariffs, and broader economic growth continues to affect investor confidence.

Regulatory scrutiny is also playing a role Telecom remains one of the most heavily regulated industries, and large transactions often require extensive approvals from competition authorities and government agencies this can add both time and complexity to potential deals.

As a result, many operators appear to be taking a more conservative approach, choosing to strengthen their existing businesses rather than pursue aggressive expansion through acquisitions.

Asset Sales Take Centre Stage

One of the most notable findings from Bain’s report is the growing importance of divestments Asset sales accounted for 53% of total telecom M&A value during the first quarter of 2026, making them the largest contributor to deal activity during the period.

This trend reflects a broader shift across the telecom industry rather than buying new businesses, operators are increasingly selling non-core assets and streamlining portfolios such transactions allow companies to raise capital, reduce debt, and focus resources on areas that offer stronger long-term growth potential.

Also Read: Reliance Jio IPO Could See Stake Sales by Meta, Google and Global Funds: Report

Many telecom operators have spent the past few years evaluating which assets are essential to their future strategy businesses that no longer align with core objectives are increasingly being sold or spun off, creating a steady flow of divestment-related activity even as traditional M&A remains weak.

Infrastructure Deals Continue to Dominate

The report also highlights the continued importance of scale and infrastructure transactions according to Bain, scale and infrastructure deals have accounted for more than 70% of total telecom M&A value over the past five years this indicates that investors and operators continue to see long-term value in assets such as towers, fibre networks, data centres, and other critical communications infrastructure.

Demand for digital connectivity continues to grow globally, driven by cloud services, artificial intelligence applications, enterprise digital transformation, and increasing data consumption as a result, infrastructure assets remain attractive investment targets even during periods of broader market uncertainty.

The continued dominance of infrastructure-focused deals suggests that while overall telecom M&A activity may be slowing, strategic investment in foundational network assets remains a priority.

Scope Deals Gain Momentum

Another notable trend identified in the report is the rise of scope deals scope transactions accounted for 23% of total telecom deal value in the first quarter of 2026, up significantly from 11% a year earlier these deals typically involve operators expanding into adjacent markets, services, or capabilities rather than pursuing traditional scale-driven acquisitions.

The increase suggests that telecom companies are looking for targeted opportunities that can strengthen existing businesses without requiring the financial commitment associated with large mergers.

Where Telecom Investment Is Heading Next

Bain expects telecom M&A activity to remain relatively stagnant in the near term persistent macroeconomic uncertainty, elevated financing costs, regulatory challenges, and ongoing trade risks are likely to continue affecting dealmaking decisions. However, the underlying need for network investment and digital infrastructure development remains strong.

For now, the message from the telecom industry appears clear rather than pursuing headline-grabbing acquisitions, many operators are focusing on portfolio optimization, infrastructure investment, and selective strategic transactions in a challenging market environment, preserving flexibility and strengthening core operations may prove more valuable than chasing the next big deal.

If this article saved you time or helped you decide better, consider supporting our work.

FAQs

What happened to global telecom M&A activity in Q1 2026?

Global telecom M&A deal value fell 18% year-on-year, declining from $16 billion in Q1 2025 to $13 billion in Q1 2026.

Why did telecom M&A activity decline?

Higher interest rates, economic uncertainty, regulatory challenges, and trade-related concerns contributed to slower dealmaking activity.

What were the biggest telecom deals in Q1 2026?

According to Bain, asset sales and infrastructure-related transactions accounted for the majority of telecom deal value during the quarter.

Why are telecom operators focusing on asset sales?

Asset sales help operators raise capital, reduce debt, simplify operations, and focus on core growth areas.

Which telecom assets remain attractive to investors?

Telecom towers, fibre networks, data centres, and other digital infrastructure assets continue to attract investment interest.