Andrew Bonwick

Vice President of Product Development at Relm Insurance

Madhav Sheth

CEO of Ai+ Smartphone

Varun Kashyap & Sridevi Reddy

Co-Founders, Zithara.ai

Transforming Indian Offline Retail and Customer Engagement Using AI

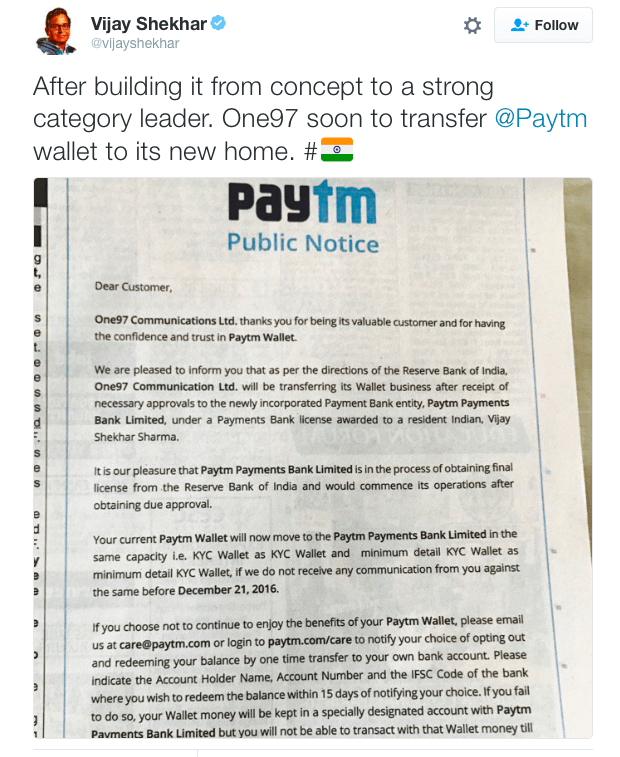

PayTM is soon going to merge its PayTM Wallet business with its PayTM Payments Bank division. The company is waiting for RBI’s green signal to start its banking operations.

- Make Telecom Talk My Trusted Source

The parent company of PayTM – One 97 Communications is still going to carry on other e-commerce activities on PayTM’s online portal. However, the wallet service will be merged into PayTM’s future banking business. It is noteworthy to point out that PayTM’s bank division’s license is owned by PayTM’s founder – Vijay Shekhar, not One 97 Communications.

PayTM incorporated PayTM Payments Bank Ltd and PayTM E-commerce Pvt. Ltd as different entities in August. Many reports also suggest that PayTM’s e-commerce portal might act as an operating base for AliBaba’s operations in India.

What will happen to your PayTM Wallet and Existing Balance?

As mentioned above, PayTM Wallets will now be a part of PayTM Payments Bank Ltd. As per PayTM’s public statement, the current PayTM wallet owners can login into PayTM account and transfer their existing balance to their bank accounts by providing bank details (Account Number and IFSC code). The company is giving a 15-day time period to wallet owners to transfer their Wallet balance to Bank accounts (till December 21). For the ones who fail to do so, the balance will be transferred to a specialised account in PayTM Bank but they will not be able to transact until they provide their bank details.

Also, the above process is not applicable for the users whose PayTM wallet has been inactive for last six months with zero balance. Such users will have to login into their PayTM account and send a written consent via e-mail or in-app option to get included in PayTM Payments Bank Ltd.

PayTM Bank: License and Operative Capacity

A spokeswoman for PayTM told Economic Times,”As per the directions of RBI; the company will transfer its wallet business to the newly incorporated PayTM Payments Bank Limited (PPBL) after receipt of necessary approvals. The (payments bank) is in the process of obtaining final licence from RBI and will commence operations after obtaining due approvals” she said. But she did not reveal anything about Alibaba and PayTM’s collaboration, terming it as a mere “speculation”.